Global carbon capture capacity due to rise sixfold by 2030

More than $3 billion has been invested in carbon capture so far in 2022

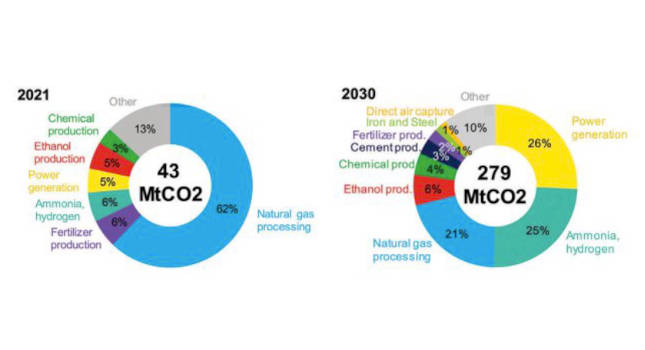

The global capacity for carbon capture in 2030 is set to increase sixfold from today’s level, to 279 million tons of CO2 captured per year, according to research company BloombergNEF’s (BNEF) newly released 2022 CCUS[1] Market Outlook. Drastic growth in the market has led to a 44% increase in expected 2030 capacity compared to last year’s outlook.

Carbon capture, utilization and storage (CCUS) is a key technology needed to decarbonize hard-to-abate sectors such as petrochemicals and cement, and to provide 24/7 clean power through gas plants fitted with capture equipment. Still, despite significant acceleration in the sector in the past two years, the world’s capacity for carbon capture is not being deployed fast enough to meet climate goals at the end of the decade, according to BNEF research.

Today, most capture capacity is used to collect carbon dioxide (CO2) from natural gas processing plants and used for enhanced oil recovery. By 2030, most capture capacity will be used for the power sector, for the manufacture of low-carbon hydrogen and ammonia, or to abate emissions from industrial sources (See figure 1).

The amount of CO2 being captured today is 43 million tons, or 0.1% of global emissions. If all the likely projects that have been announced come online, there would be 279 million tons of CO2 captured every year by 2030, accounting for 0.6% of today’s emissions.

The destination for captured CO2 is also due to change significantly from the status quo. In 2021, some 73% of captured CO2 went to enhanced oil recovery operations. By 2030, storing CO2 deep underground will overtake oil recovery as the primary destination for CO2, with 66% of it going to dedicated storage sites. This change is being driven by legislation that incentivizes storage over CO2 utilization, and by projects that aim to use carbon capture and storage (CCS) as a decarbonization route and must store the CO2 to meet their goals.

“CCS is starting to overcome its bad reputation,” said David Lluis Madrid, CCUS analyst at BNEF and lead author of the report. “It is now being deployed as a decarbonization tool, which means the CO2 needs to be stored. A lack of CO2 transport and storage sites near industrial or power generation point sources could be a major bottleneck to CCS development. But we are already seeing a big increase in these projects to serve that need.”

Despite rapid growth in capture project announcements, the industry is still far from making a dent in global emissions. In order to be on track for net-zero and less than 2 degrees Celsius of warming by 2050, between one and two billion tons of CO2 would need to be captured in 2030, an order of magnitude higher than current plans. Legislators have recognized this mismatch and are ramping up their support for the industry.

The Inflation Reduction Act passed in the US increased tax credits for CCUS by 70%, making a viable business case for the technology in petrochemicals, steel, cement, and in some regions, power. Incentives like these mean that countries, such as the US, will remain global leaders for CCUS. The US tax credits are now very generous, and the law is set to supercharge project announcements in the ethanol and petrochemicals sectors, as well as in direct air capture (DAC), to provide high-quality carbon offsets for the voluntary market.

Original content can be found at Oil and Gas Engineering.

Do you have experience and expertise with the topics mentioned in this content? You should consider contributing to our CFE Media editorial team and getting the recognition you and your company deserve. Click here to start this process.

Related Resources